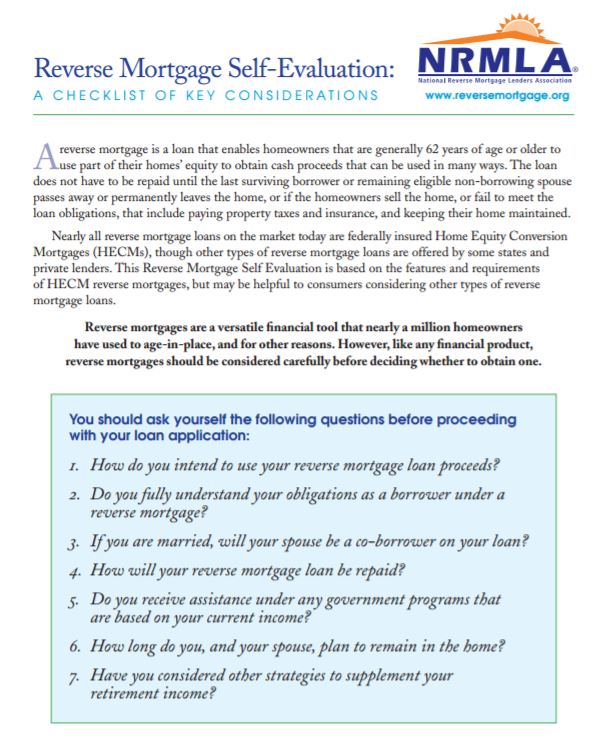

Colorado Springs Reverse Mortgages General Information

What is a reverse mortgage?

Colorado Springs Reverse Mortgages General Information: A Colorado reverse mortgage is a federally regulated program for homeowners, aged 62 and older. It allows the equity in your home to pay you rather than you paying for the home.

What is a Government Insured HECM program?

HECM stands for Home Equity Conversion Mortgage. It is a federally insured and guaranteed program. The HECM is a safe way for you to access the equity in your home without ever making a mortgage payment.

How is this program safe for senior homeowners?

No matter what happens in the economy, how much money you receive, or how long you live in your home you will never be required to make a mortgage payment. In addition, no matter what happens to your lender or your home’s value you have guaranteed access to your money.

Who owns the home if I take a reverse mortgage?

You own the home. However, you pledge the home as collateral.

What happens if, in the future, the loan exceeds the value of the home?

Your reverse mortgage will continue - thanks to the federal insurance. The line of credit will still be available and monthly disbursements you may have set up will still be sent to you.

How are reverse mortgages different today?

Today’s reverse mortgages are highly regulated by Steve and Federal laws to make then safe and to protect you. Among others, the following regulations apply:

- You retain title of the home.

- No equity share is allowed, meaning the lender does not slowly take over your home.

- Fees and costs are federally regulated.

How does a reverse mortgage compare to a conventional mortgage?

IN a conventional forward mortgage, you make monthly payments to the bank, eventually paying off the mortgage over time. With a reverse mortgage, you receive cash from your lender, as lump sum upfront, as monthly installments or as a line of credit that grows over time. As long as you live in your home, you never have to pay off a single dollar of the loan.

What restrictions apply to the cash I receive from a reverse mortgage?

It is your money and you can use it the way you want. It is non-taxable, and does not affect social security payments. We recommend that you talk with a competent financial advisor to determine the effect on any other benefits you may be receiving.

When does a reverse mortgage become due, and what happens then?

When you no longer live in your home, or when you pass away, the reverse mortgage becomes due. You or your heirs have two options:

- Pay off the reverse mortgage, including the accrued interest and retain ownership.

- Give up ownership of the home and receive the difference between the net sales proceeds and the loan balance. You will not be liable for any shortfall if the sales proceeds do not cover the loan.

Your loan may also become due and payable if you do not continue meeting the terms of the loan. (For example, paying taxes and insurance owed on the property.)

Read more at: http://www.reversevision.com

IN THE PRESS: Reverse Mortgage is Smart Money?

IN THE PRESS: Reverse Mortgage is Smart Money?

Many

Many

{kind=link}