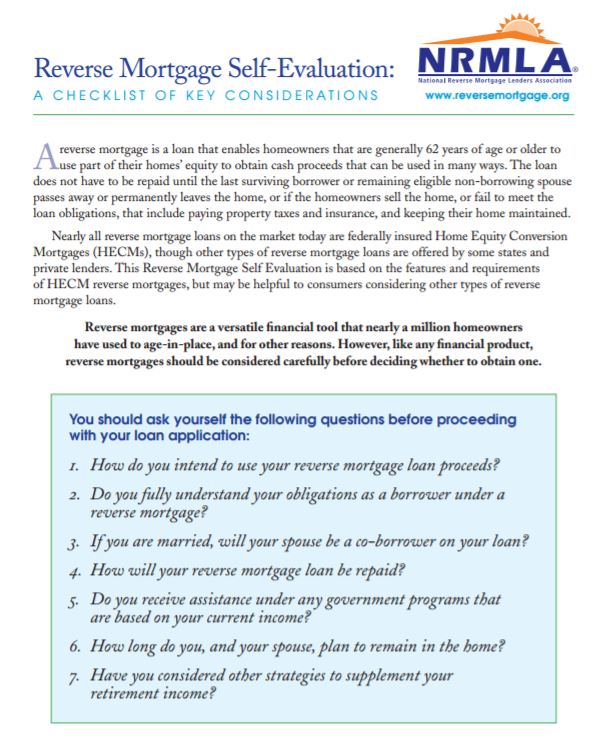

A Checklist of Key Considerations

Reverse Mortgage Self-Evaluation: Reverse mortgages are a versatile financial tool that nearly a million homeowners have used to age-in place, and for other reasons. However, like any financial product, reverse mortgages should be considered carefully before deciding whether to obtain one.

The six-page Reverse Mortgage Self-Evaluation: A Checklist of Key Considerations was created to help senior homeowners consider whether a reverse mortgage is right for them. This guide is best shared during the pre-application phase so that consumers can discuss any questions with their HUD-approved reverse mortgage counselor.

The Self-Evaluation is also posted on NRMLA’s consumer education website at www.reversemortgage.org/Checklist.

The seven questions below, plus additional considerations and information about reverse mortgage loans, are included in NRMLA’s Reverse Mortgage Self-Evaluation.Download and print a free copy of the Checklist here.

1. How do you intend to use your reverse mortgage loan proceeds?

One of the advantages of a reverse mortgage loan is that borrowers generally have the freedom to use their cash proceeds any way they choose. Eligible homeowners obtain reverse mortgages for many reasons.

Reverse mortgage loans are most successful when borrowers have a plan to ensure the money supports and sustains them for as long as they want to stay in their home. Additional consumer protections were put into place in 2013 to help borrowers preserve more of their home equity during the first year of the loan.

- Do you have a plan for making your reverse mortgage loan proceeds last?

2. Do you fully understand your obligations as a borrower under a reverse mortgage?

Reverse mortgage borrowers are not required to make monthly loan payments to their lender, but must continue to meet certain obligations in order to stay current on the loan. Failure to meet these obligations may result in the loan becoming due and payable.

- Will you live in your home for the majority of the calendar year?

- Are you prepared to maintain the condition of your property?

- Will you be able to pay your property taxes, insurance, and homeowner fees?

- Do you understand what will happen if you cannot pay your taxes, insurance, or homeowner fees?

- Do you understand your personal finances will be reviewed?

3. If you are married, will your spouse be a co-borrower on your loan?

Under the rules of a HECM reverse mortgage, borrowers must be at least 62 years old, named on the title of the home, and use the home as their principal residence. Spouses who do not meet these criteria cannot sign the HECM reverse mortgage loan documents as a borrower and will be identified as either an eligible non-borrowing spouse or an ineligible non-borrowing spouse depending on certain additional criteria. You should speak to your HUD-approved reverse mortgage counselor about the non-borrowing spouse criteria.

- What if your co-borrower spouse survives you?

- What if your eligible non-borrowing spouse survives you?

- What if your ineligible non-borrowing spouse survives you?

4. How will your reverse mortgage loan be repaid?

A reverse mortgage is a non-recourse loan which means that the borrower or the borrower’s estate will never be obligated to pay the lender more than the loan balance or the current value of the home, whichever is less. When a loan is called due and payable, the reverse mortgage borrower or the borrower’s estate only needs to repay the lesser of either the loan balance or 95% of the home’s appraised value at that time.

- Do you know your options for repaying the loan?

- Do you want someone to inherit your home after you pass away?

- Did you know that you can prepay your reverse mortgage loan?

5. Do you receive assistance under any government programs that are based on your current income?

A reverse mortgage does not affect regular Social Security or Medicare benefits. However, if you are on Medicaid or receive Supplemental Security Income (SSI), reverse mortgage proceeds may affect your benefits.

- Are you considering a lump sum cash draw?

6. How long do you, and your spouse, plan to remain in the home?

Reverse mortgages, like many financial products, have costs associated with them, including some that need to be paid up-front when the reverse mortgage is obtained. Among other things, that means that if you or your spouse are not likely to continue to live in your home for more than several years after the reverse mortgage is obtained, you should pay particular attention to those costs and consider them carefully with your HUD-approved reverse mortgage counselor and whether there may be other more cost effective alternative strategies.

7. Have you considered other strategies to supplement your retirement income?

- Do you qualify for public or private benefits available to low-income people with Medicare?

- Did you know there are other ways to tap your home equity?